The B2B payments space has seen phenomenal growth over the last few years. It is no secret that the COVID crisis has accelerated growth in the B2B payments sector. Contactless payments to in-cart credit options, the market is rife with novel payment solutions launched more frequently.

While many B2B companies continue to rely on quintessential payment options such as equipment leasing, there have been new categories created in this space known as Buy-Now-Pay-Later (BNPL) solutions which have gained popularity.

The implementation of a BNPL solution or equipment leasing is a strategic investment for any B2B business. Selecting the right payment option and choosing the right vendor is key to business success.

With multiple B2B payment options available in the market, it has become rather confusing as to what they do and their purpose and benefits. In a bid to bring more clarity on these two B2B payment solutions, this article elucidates their differences and benefits.

Equipment Financing

Small businesses are usually on a shoestring budget and purchasing equipment means parking a significant amount thereby making it difficult to have everything up and running smoothly in a short time. This is where equipment financing comes to their rescue. Instead of paying the entire amount upfront, the business can opt for equipment leasing and pay as monthly charges, sometimes which are also spread out over several years.

The key benefit of selecting an equipment financing partner is that businesses can offer flexible payment terms to their business buyers for large purchases without having to wait on payments, instead they immediately receive payment for the order. This of course in turn improves cash flow and working capital.

Business owners also mitigate the payment risks associated with extending credit to their business buyers. Once a buyer is approved for the loan and the payment is made to the supplier, the merchant no longer needs to worry about defaults or bad debt on that purchase.

The largest benefit to offering equipment financing to your business buyers is the ability to quite easily increase your average order value and sell more large ticket items. With that said, equipment financing is best suited for items that a business may need more than 12 months to pay for. For that reason, equipment financing is used on a low percentage of sales orders, smaller price tag orders like parts or services are typically managed through other payment channels.

It is important to note that despite the economic slowdown in 2020, the Equipment and Software (E&S) investment surged 21%, providing a strong jump-off point for 2021. According to the 2021 Equipment Leasing and Finance US Economic Outlook Report, E&S investment growth sustained its rebound through the end of 2020.

Equipment Financing

Pros

- No cash flow concerns

- No payment risk

- Automated credit approvals

- Drastic increase in sales in comparison to credit card / cash payments

Cons

- Typically not utilized by enterprise buyers

- Low frequency use

Typical use case:

- For businesses that sell large ticket items that their buyers need years to pay off (typical large machinery)

Typical buyer base:

- Small businesses that need a significant loan to purchase a one time purchase.

Buy Now Pay Later

In simple words, the BNPL model is very similar to equipment financing - it is just usually quicker, more integrated, and intended for purchases that do not need years to pay off.. It comes with the same financial advantages, such as increased liquidity and cash flow.

Buy Now, Pay Later B2B payment solutions are utilized most by suppliers selling to small businesses that have large ticket items/ order sizes that are typically too large for the Credit Card but are not big enough to take more than a year to pay off. As an example, this could be a commercial oven for a restaurant.

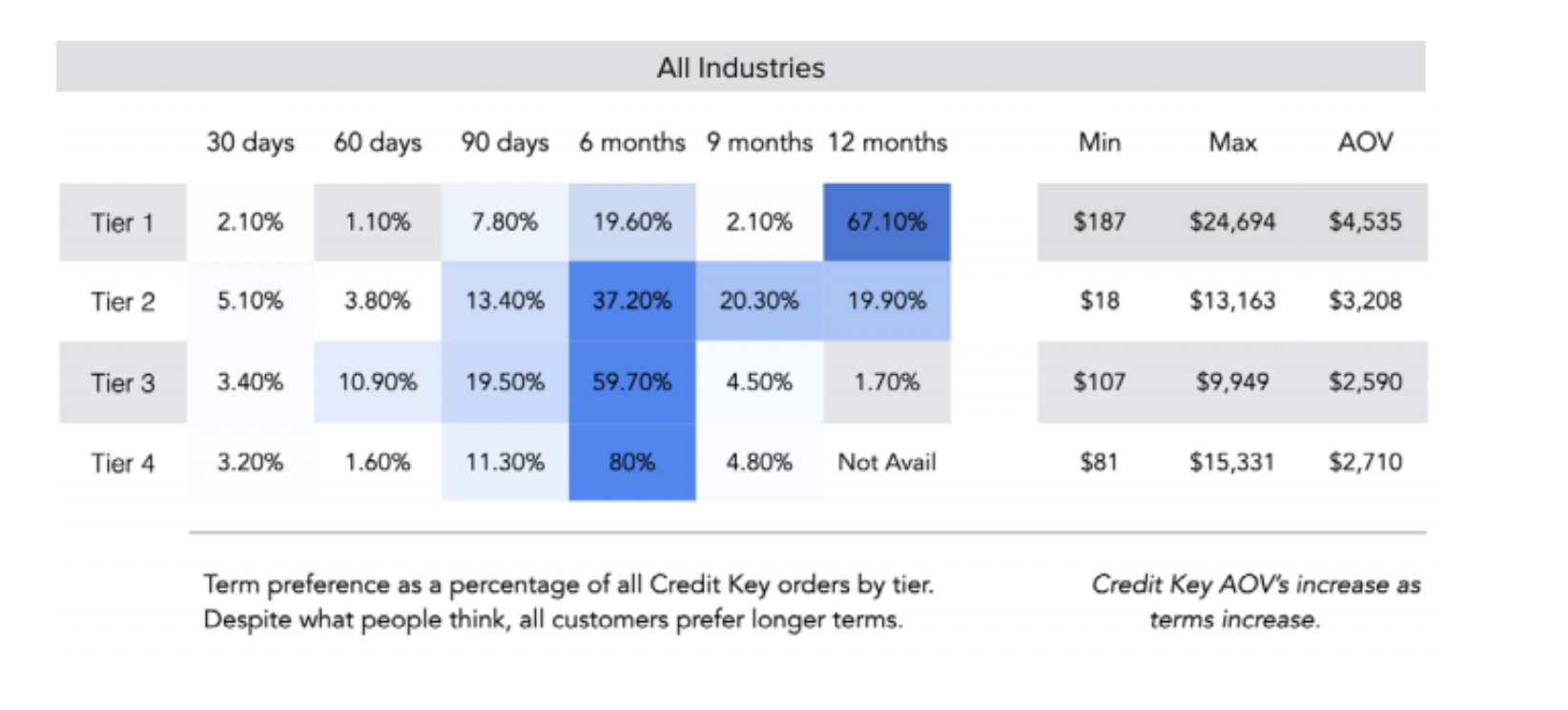

See below for typical terms selected and order sizes for Buy Now, Pay Later B2B purchases:

Source: Key Insights Report

The process of applying for a BNPL is significantly less time consuming and intensive than a traditional loan or equipment financing. The approval process is instant and can be done right from checkout. This makes it the preferred method of payment for businesses looking to buy immediate goods, especially online, that are larger than their typical day to day transactions.

With platforms such as Credit Key (the only Buy Now, Pay Later exclusive to B2B transactions), businesses buyers can benefit from flexible payment options by paying as little as 0% over the first 30 days or selecting up to 12 months' terms right from checkout.

Due to offering smaller installments for large orders, small business buyers are able to afford more expensive purchases. This leads to merchants having an increase in conversion rates, Average Order Value, and order frequency.

Buy Now, Pay Later

Buy now pay later solutions to offer immediate approvals and flexibility for small business buyers. Giving them the ability to pay off purchases in 30 days risk-free or extend payments out to 12 months.

Pros

- No cash flow concerns

- No payment risk

- Instant and fully automated credit approvals

- A drastic increase in sales in comparison to credit card/cash payments

- Increase in conversion rates

Cons

- Typically not utilized by enterprise buyers

Typical use case:

- For businesses looking to actively automate and increase their SMB customer spending with their business.

Typical buyer base:

- Small businesses that need to make larger orders for their business.

Summary

While all buyer circumstances are different, there are some similarities that most of them fall under. It is important to understand if your business requires a BNLP solution and/or equipment financing and what impact its deployment will have on your business.

Below is the quick summary of the BNPL vs Equipment Financing payment option

|

Benefit |

Buy Now, Pay Later |

Equipment Financing |

|

Credit Terms |

30 days to 12 months |

12 to 60 months |

|

Approval Speed |

Instant |

2 - 48 hours |

|

Integrations |

Payment & Checkout Integration |

No Integration |

|

Size of Credit Line |

Instant $50k, up to $200k |

Up to $500k |

|

Payment Risk |

No Payment Risk |

Varies depending on the provider |

|

Human Resources |

No employees needed |

No employees needed |

|

Cash Flow |

Paid within days of purchase |

Paid within days of purchase |

|

Order Value |

Drastic growth over credit cards |

Drastic growth over credit cards |

Topics from this blog: B2B Payments