The B2B payments landscape is going through rapid expansion with novel offerings by new companies in the financial space. While many are very innovative for the space, there is also a noticeable trend that needs to be acknowledged. There is no doubt that B2C payments have evolved before B2B and it continues to be a leading indicator for where B2B payment trends will eventually end up. Payment options like Venmo, Affirm, Klarna, and Sezzle have gone from unknown brands just years ago into household names.

The trend that most people ignore is the idea that all consumers, even those working for B2B organizations, have seen these new offerings and are looking for them in how they do business. With B2C payment options evolving around great user experience, speed, and convenience, the B2B payment trends are evolving to match the same benefits as the B2C counterpart.

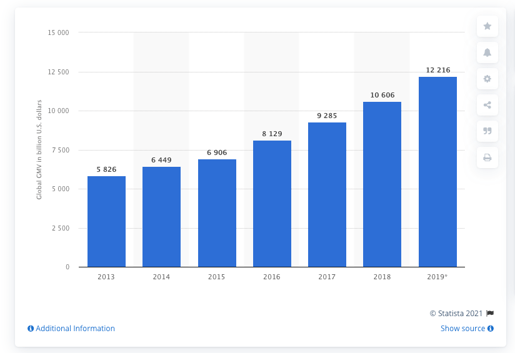

After B2C payments growth, the outlook for the B2B payments growth is equally positive in the years to come. According to a report on Statista the gross merchandise volume of B2B e-commerce transactions increased from $5.8 trillion in 2013 to $12.2 trillion in 2019, and in the U.S, checks now account for around 40% of B2B transactions, compared with 80% in 2014. This article will point out some of the key trends and predict what is yet to come.

Source-Statista Report

Source-Statista Report

Accounts Receivable

Accounts receivable has been associated with consumers for a long time now. In the 1950’s, patrons of restaurants would be able to put their meals on a tab and then pay the total bill by the end of the month. Of course this was a headache for the restaurant to manage and an inconvenience for the consumer. In 1958, Bank of America was the first to launch a revolving line of credit to the people that banked with them. Allowing customers of restaurants to buy the items they wish on a line of credit and moving the Accounts Receivable from the restaurant back to the bank. Transforming the consumer world into what it is today, full of Credit cards and less cash payments.

Today’s B2B transactions are largely still done by invoicing and paper checks but is rapidly transforming itself to automated payment options through Credit Management programs, automated accounts receivable software, and digital payments. Companies are recognizing the work it takes to manage their own receivables program and the frustration it brings to their customer base. Using Credit Management software has drastically decreased the cost of extending credit to business customers in both capital and human resources.

Large Purchase Financing

Consumers are impatient. Usually when you want to purchase something, especially an item where people have invested a lot of time researching the item, they prefer a quick transaction. For the longest time this wasn’t the case. Consumers would need to go to the bank, talk to a banker to see if they can get the loan they need for a purchase and then relay that to their purchase. This doubled the effort of buying any large item.

This has changed drastically over the last couple years, as companies like Synchrony Bank, have streamlined the process of getting a simple loan to pay off home improvements, furniture, and other large purchases. Applications and approvals are done in minutes electronically allowing for a consumer to make quick purchases on the large ticket items they need. This transition is slowly starting to take place in B2B with Equipment financing. What used to be a long application process outside of the company’s sales cycle is now becoming a more integrated process - especially with e-commerce.

Buy Now, Pay Later

Buy Now,Pay Later payment model has caught on like wildfire in the consumer space. It met a consumer need that was largely unsatisfied just a couple years ago. The need is for consumers that want a particular product that is outside their typical spending. In the past, this would have meant saving up for the item and buying it at a later point.

With a BNPL solution, consumers can in fact buy the product they wish to have now without negatively affecting their cash flow. This skips the process of saving, and consumers get what they want, when they want it.

Buy Now Pay Later has recently moved into B2B with Credit Key. Like consumers, there are purchases that businesses want now, but do not want to, or have the luxury, to save up for it. For example, in a restaurant, their deep fryer stops working. They could save up a couple months to buy a new one, but saving up during that time also means they are not going to be serving fried foods on their menu during that time, shrinking their revenue.

Therefore, businesses also need the ability to immediately make the purchases they need to grow their business that may be outside of their planned budget.

Summary

B2C trends determine the changing face of the B2B payments landscape. B2C industry continues to be the leading indicator what of changes B2B industry will adopt in due course of the time. Some of the areas where B2B payments follow the footsteps of the B2C payments are mentioned below:

- Accounts Receivable

- Large Purchase Financing

- Buy Now Pay Later payment model

For more information on different B2B payment solutions download the white paper

Topics from this blog: B2B Payments