For B2B companies, the right financing solution can be just what’s needed to spur massive growth.

In most cases, it all comes down to improving working capital and/or cash flow. After all, with more cash on hand, keeping your business running smoothly — and consistently growing — becomes that much easier.

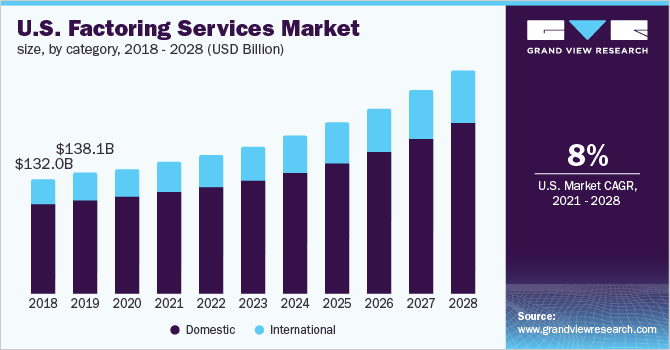

To this end, more and more B2B companies have been turning to invoice factoring services. In fact, the factoring service market has grown steadily over the last few years — and is projected to explode over the next decade.

Here’s a quick explainer of how invoice factoring works, courtesy of Excel Capital Management:

Perhaps the main reason invoice factoring has become so common is because it’s a way of receiving a substantial loan amount that isn’t based on debt. Rather, the process of invoice factoring involves selling outstanding Accounts Receivable (from open net terms programs with your customers) to a factoring company, who in turn pays your company immediately.

(Think of it like a cash advance in the B2C world.)

To be sure, invoice factoring can be a valuable financing option in certain scenarios for certain B2B companies.

But, there are a number of reasons invoice factoring may not be the best financing option for your business.

Here, we’ll take a look at the key disadvantages of invoice factoring — and discuss why Buy Now, Pay Later may be the better option for your situation.

At first glance, invoice factoring does seem like a silver bullet solution to your immediate cash flow problems.

I mean, you get paid immediately, and you don’t have to worry about paying anything back to the financing company? Sounds like a dream come true.

Unfortunately, the process is a bit more nuanced than that. Even when things go smoothly, invoice factoring may turn out to be more trouble for your company than it’s worth.

Here’s what to look out for.

Factoring companies don’t purchase invoices at full price, but rather at a fraction of the total amount owed.

Typically, they’ll pay anywhere from 50-90%, depending on factors such as:

The client, then, will only receive up to 90% of each invoice they factor upfront — and be reimbursed the rest once the invoice is paid in full (minus service fees, which we’ll discuss in a bit.)

While this is definitely preferable to collecting net payments over time, those looking to get paid in full immediately will be sorely disappointed.

You’ll also pay factoring fees of 1-5% of the amount of each invoice factored. As a service charge, factoring fees are not reimbursed — and are either taken immediately or once an invoice has been paid in full.

Simply put:

Using this method means accepting at least a 1-5% decrease on all revenue generated via factored invoices.

When a factoring company purchases an invoice, they assume — in one way or another — the responsibility of collecting the payment from the vendor’s customer.

However, factoring companies also put safeguards in place to minimize the amount of risk they take on when assuming this responsibility.

(And, in fact, some factoring companies only provide recourse factoring services, meaning the vendor is still responsible for collecting on unpaid invoices.)

These safeguards typically include:

These safeguards essentially allow factoring companies to pass certain financial risks on to your company — while still maintaining the facade of being completely risk-free.

Many invoice factoring companies also charge incredibly high fees when things don’t exactly go according to plan.

Whether it’s a missed payment from a customer, a missed revenue quota on your part — or something else entirely — you may find yourself owing your factoring company much more than you’d initially anticipated.

Of course, the best invoice factoring companies out there will be more transparent with all this info. Still, it’s crucial to put safeguards in place on your end to ensure you meet the terms of your agreement at all times — and avoid any additional fees altogether.

Again, when a factoring company purchases an invoice, they typically assume responsibility for collecting the remainder of the balance.

This includes engaging with the vendor’s customer directly on a regular basis — in essence injecting themselves into the customer experience that you provide your customers.

This...might not be a good thing.

For one, your customers might not appreciate seemingly being pawned off to a third-party company — regardless of the actual impact it will have on their experience. Secondly, the factoring company’s approach to engaging with buyers may differ completely from your own — and it might not exactly be what your buyers are looking for.

While it might not be too big of an issue for your customers, it’s still an extra risk you’ll be taking when using invoice factoring services.

The accounting process for invoice factoring is quite labor intensive.

The biggest issue:

Invoice factoring, by nature, requires multiple bookkeeping adjustments for accurate accounting purposes. Because factored invoices are paid out in two installments, there are at least two financial engagements to keep track of at all times.

It’s also a very hands-on operation, on both sides of the equation. First, the vendor must identify which invoices are to be factored, then process and deliver them to the factoring company. From there, the factoring company assesses each invoice before pricing it accordingly and submitting the initial reimbursement.

Though it’s not necessarily arduous, the invoice factoring process can potentially be a drag on your resources if you’re not prepared to handle it.

To be blunt:

A Buy Now, Pay Later is a much better financing option for B2B businesses — period.

In fact, Credit Key’s BNPL solution flips every single one of the disadvantages we just discussed on its head.

First of all, Credit Key’s clients get paid completely in full (minus a small transaction fee) within 48 hours of a purchase. There’s no waiting for the last 10, 20, or even 30% of the invoice; it’s all paid out right away.

From there, Credit Key assumes full responsibility for collecting payments from the buyer — at no risk to the client. If a problem arises regarding the buyer’s payments, Credit Key will handle it at no expense to the client.

As for customer service and experience, buyers agree to Credit Key’s terms before making the purchase — meaning their expectations are set from the start.

(They also have the option of not using Credit Key when making a purchase, as well.)

Lastly, Credit Key’s financing process occurs all within a single transaction that’s completely automated on the client’s end. This means less time spent tracking AR — and more time spent growing your business.

Want to learn more about how Credit Key’s Buy Now, Pay Later services can help improve your cash flow? Get in touch with our team today!

{kind=link}

{kind=link}